- Compliance Equity Crowdfunding Reg. CF

- Oct 31

Summary of Reg CF Rules

What Passed in the Title III Vote

Earlier today, the Securities and Exchange Commission adopted final rules for Title III of the JOBS Act. This long-anticipated step makes way for U.S. companies to raise equity and debt capital from accredited and non-accredited investors through CrowdFunding in a simplified and hopefully, more cost-effective manner.

The final rules, Regulation Crowdfunding, permit individuals to invest in securities-based crowdfunding transactions subject to certain investment limits. The rules also limit the amount of money an issuer can raise using the crowdfunding exemption, impose disclosure requirements on issuers for certain information about their business and securities offering, and create a regulatory framework for the broker-dealers and funding Platforms that facilitate the crowdfunding transactions.

Below are the highlights of the recommended Final Rules from the SEC Press Release issued earlier today:

Company Limitations

- A company may raise a maximum aggregate amount of $1.07 million through crowdfunding offerings in a 12-month period;

- During the 12-month period, the aggregate amount of securities sold to an investor through all crowdfunding offerings may not exceed $107,000.

- Certain companies would not be eligible to use the exemption, including:

- Non-U.S. companies,

- Exchange Act reporting companies,

- Certain investment companies,

- Companies that are subject to disqualification under Regulation Crowdfunding,

- Companies that have failed to comply with the annual reporting requirements under Regulation Crowdfunding during the two years immediately preceding the filing of the offering statement, and

- Companies that have no specific business plan or have indicated that their business plan is to engage in a merger or acquisition with an unidentified company or companies (no blank check companies).

Investor Limitations

- Individual investors may, over a 12-month period, to invest in the aggregate across all crowdfunding offerings up to:

- If either their annual income or net worth is less than $107,000 than the greater of:

- $2,200 or

- 5 percent of the lesser of their annual income or net worth.

- If both their annual income and net worth are equal to or more than $107,000, 10 percent of the lesser of their annual income or net worth;

- If either their annual income or net worth is less than $107,000 than the greater of:

- Securities purchased in a crowdfunding transaction generally are restricted and may not be resold for one year.

- Holders of these securities would not count toward the threshold that requires a company to register its securities under Exchange Act Section 12(g) if the company is current in its annual reporting obligations, retains the services of a registered transfer agent and has less than $25 million in total assets as of the end of its most recently completed fiscal year.

- All transactions relying on the new rules would be required to take place through an SEC-registered intermediary, either a broker-dealer or a funding Platform.

Company Disclosure Requirements

- Companies that rely on the recommended rules to conduct a crowdfunding offering must file certain information with the Commission and provide this information to investors and the intermediary facilitating the offering, including among other things:

- Information regarding the price and pricing method of the securities and the targeted offering price;

- A discussion of the company’s financial condition;

- financial statements of the company that, depending on the amount offered and sold during a 12-month period, are accompanied by information from the company’s tax returns, reviewed by an independent public accountant, or audited by an independent auditor.

- A company offering more than $500,000 but not more than $1.07 million of securities relying on these rules for the first time would be permitted to provide reviewed rather than audited financial statements unless financial statements of the company are available that have been audited by an independent auditor;

- A description of the business and the use of proceeds from the offering;

- Information about officers and directors as well as owners of 20 percent or more of the company; and

- Certain related-party transactions.

- Companies relying on the crowdfunding exemption would be required to file an annual report with the Commission and provide it to investors.

Crowdfunding Platform/Intermediary Rules

- Funding Platforms must register with the Commission on new Form Funding Platform, and become a member of a national securities association (currently, FINRA). A company relying on the rules would be required to conduct its offering exclusively through one intermediary platform at a time. Such Funding Platforms/Intermediaries would be required to undertake the following:

- Provide investors with educational materials that explain, among other things, the process for investing on the platform, the types of securities being offered and information a company must provide to investors, resale restrictions, and investment limits;

- Take certain measures to reduce the risk of fraud, including having a reasonable basis for believing that a company complies with Regulation Crowdfunding and that the company has established means to keep accurate records of securities holders;

- Make information that a company is required to disclose available to the public on its platform throughout the offering period and for a minimum of 21 days before any security may be sold in the offering;

- Provide communication channels to permit discussions about offerings on the platform;

- Provide disclosure to investors about the compensation the intermediary receives;

- Accept an investment commitment from an investor only after that investor has opened an account;

- Have a reasonable basis for believing an investor complies with the investment limitations;

- Provide investors notices once they have made investment commitments and confirmations at or before completion of a transaction;

- Comply with maintenance and transmission of funds requirements; and

- Comply with completion, cancellation, and reconfirmation of offerings requirements.

- The rules also would prohibit intermediaries from engaging in certain activities, such as:

- Providing access to companies that they have a reasonable basis for believing have the potential for fraud or other investor protection concerns;

- Having a financial interest in a company that is offering or selling securities on its platform unless the intermediary receives the financial interest as compensation for the services, subject to certain conditions; and

- Compensating any person for providing the intermediary with personally identifiable information of any investor or potential investor.

- Funding Platforms would also be prohibited from providing investment advice or making recommendations.

Regulation Crowdfunding will also contain certain intermediary specific rules consistent with their more limited activities than that of a registered broker-dealer. The rules would prohibit funding Platforms from, among other things: offering investment advice or making recommendations; soliciting purchases, sales or offers to buy securities; compensating promoters and other persons for solicitations or based on the sale of securities; and holding, possessing, or handling investor funds or securities.

The new rules and forms would be effective 180 days after they are published in the Federal Register, except that the forms enabling funding Platforms to register with the Commission would be effective January 29, 2016.

J. Martin Tate

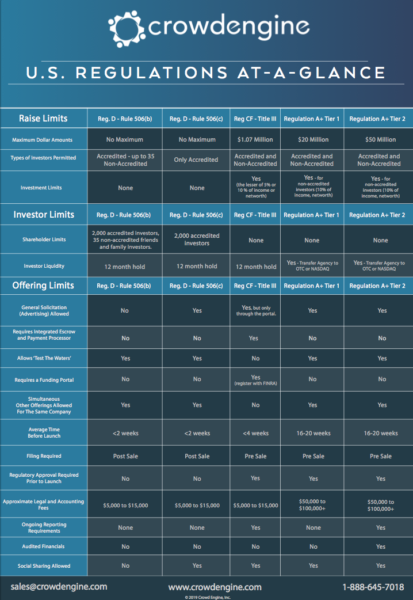

Regulations At-A-Glance

Questions about regulations? Download our Regulations at a Glance guide for free.